The New Border Is Not at the Airport

In this article:

For most of modern history, you knew exactly when you were crossing a border.

There was a queue, a passport desk, a customs officer in uniform, a stamp in your passport, and perhaps a few awkward questions about your destination, your plans, and what you were carrying. The border had a physical location. You could point to it on a map. You could feel the shift in the air the moment you stepped into the airport hall.

But borders were never only lines on maps. Medieval merchants figured this out centuries before banking apps and compliance departments existed. Along Europe’s great trade routes, certain towns held what were called staple rights. Your boat could sail freely down the Rhine. Your feet could keep walking the road. Yet at these choke points your cargo met an invisible wall: unload, sell locally through the town’s brokers, pay the toll, and only then were you allowed to continue.

Cologne was a real pro at this racket. It sat smack in the middle of one of the busiest arteries on the continent and basically said, “Your goods belong to our market first, pal”. The merchant could keep walking. His wealth? Not so much. Funny how that pattern never really died; it just got better PR.

Today the checkpoint sends you an email titled “Account Activity Review”. Your transfer is suddenly “under review”. Your withdrawal is frozen. Your custodian needs “additional information” before it can release your own money. And the bank has decided, in its infinite wisdom, that your activity no longer fits its “risk appetite”.

You sail through airport security without a second glance. Your capital doesn't. That is the new border. And guess what? It’s far more effective than any passport desk ever was, because you don’t even see it until your money is already in handcuffs.

And every institution moving value is being turned into one of these new border posts for the fiat system: banks, exchanges, payment processors, custodians, correspondent networks, KYC databases, the whole permissioned circus. That’s the part worth remembering. The rails your money still depends on are controlled by the same monetary bureaucrats who raid your savings like it is their birthright and dress it up as “prudent economic leadership”.

Your body can be halfway across the planet in hours. Your wealth is still waiting for someone else’s approval. The real border is no longer the one stamped in your passport. It is the one built into the rails your money still depends on.

Sanctions Are Becoming Infrastructure Commands

In the last few weeks, the US and the UK handed us a textbook demonstration of exactly how the new border operates.

The US Treasury sanctioned four Iran-based digital asset exchanges: Nobitex, Wallex, Bitpin, and Ramzinex. The UK went after Russia-linked platforms, banks, and payment networks. Asset freezes, blocked correspondent relationships, the usual toolkit. Before anyone starts rehearsing their “but they are the bad guys” speech, save it. That isn’t the point here.

The point is that sanctions have evolved from diplomatic theater into infrastructure commands, which are injected straight into the financial machine. Banks get the memo. Exchanges get the memo. Payment processors, stablecoin issuers, compliance vendors, custodians, and correspondent networks all get the memo.

Then the predictable circus kicks off. Risk departments hit the panic button and do what they always do best: block everything first and ask questions sometime around the heat death of the universe.

The Risk Is Not Being the Target.

The comforting lie behind every permissioned system is that ordinary people have nothing to worry about.

This is why modern financial control is so slippery. It doesn’t need to accuse every person, freeze every account, or investigate every transaction directly, because that would be far too much work for the clipboard priesthood. Instead, it simply marks a route as contaminated and then watches every nearby institution scramble to prove it is standing far enough away from the smell.

A platform gets designated and suddenly nobody wants to touch any flows even remotely connected to it. A bank shows up in the wrong network and counterparties start backing away like it is contagious. A payment path brushes against the wrong jurisdiction and turns into an instant compliance migraine. A customer who was perfectly boring yesterday becomes a file, a ticket, a full review, and three pointless document requests that nobody will ever properly read.

That is the real blast radius: not direct punishment for being the target, but punishment for being close enough to make some risk officer break into a nervous sweat. Once that fear enters the system, it spreads like mold, quietly, defensively, and always further than any official press release has ever admitted.

This is how financial access becomes political. Your withdrawal requires “enhanced due diligence”. Your payment has been delayed by a banking partner. Your custodian needs another document. Your transfer cannot be completed at this time. Everyone is polite, but nobody is responsible, and “your” money sits in a queue waiting for permission to exist.

The bank blames policy. The exchange blames compliance. The custodian blames due diligence. The payment processor blames its banking partner. The banking partner blames regulatory exposure. The regulator points to guidance. Everyone is very sorry for the inconvenience, which is always touching when it isn’t their life being jammed into the machinery. But underneath the polite language, the message is brutally simple: your money can only move if every permissioned layer between you and the final settlement stays comfortable.

That cannot seriously be called ownership.

Legal Access Is Not the Same as Practical Access

This is the part the fiat system hides behind its most exhausting technicality.

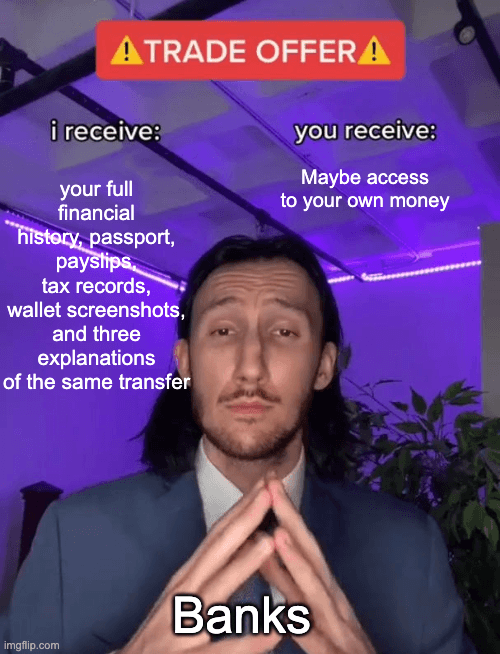

On paper, nothing has been taken from you. Your account still exists, your balance still appears on the screen, your assets are still “available”, and some customer support script will cheerfully remind you that all reviews are carried out in accordance with internal policy and applicable regulation, which is bureaucrat-speak for “please stop bothering us about when you can actually use your own damn money”.

The trick is that ownership doesn’t need to be formally revoked for access to become completely useless. A transfer can be delayed at the exact moment you need it most. A withdrawal can be placed behind another review. A bank can ask for the same documents you already sent twice. A platform can change limits and restrict activity. Nothing has to be confiscated in the old dramatic sense, because friction does the heavy lifting all by itself.

That is the crucial gap between legal access and practical access. Legal access is the comforting fiction printed in the terms and conditions. Practical access is whether the money moves when you need it, in the amount you need, through the route you need, without having to beg a chain of intermediaries.

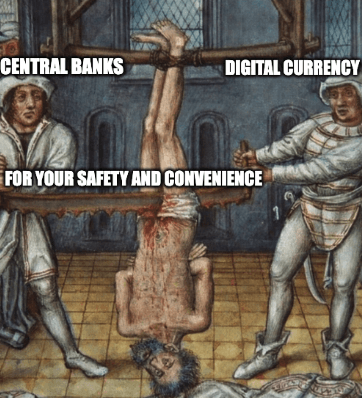

And this is exactly why the global CBDC obsession should terrify anyone who still believes in genuine ownership of money. These are not innocent upgrades to the payment system. CBDCs are the final boss of fiat control: fully programmable, instantly traceable, centrally steerable money. They let governments impose negative interest rates with a casual keystroke, make funds expire like old milk if you don’t spend them fast enough, lock your spending to approved merchants or postcodes, or freeze your balance the second your transaction pattern looks a bit too independent. No more hiding behind slow, leaky banks. The leash goes straight from the central planner’s desk to your wallet.

They’ll call it “modernization” and “financial inclusion”, of course. Save too much for a rainy day? We’ll just make it depreciate faster for your own good or even put an expiry date on it. Spend on the wrong things? We can route-restrict that. Step out of line politically or behaviorally? Watch how quickly your money decides to take a little nap. This is the transformation of money into a behavior-modification app with a few extra steps.

Today the friction comes through banks, processors, custodians, and compliance departments. A CBDC perfects and weaponizes it, removing the last annoying distance between a bureaucrat’s bright idea and the contents of your pocket.

This is why “but I still legally own it” is such hollow, laughable comfort. The more money becomes programmable, fully surveillable, and dependent on approved digital rails, the less ownership actually means. Practical access can be shaped, throttled, redirected, or revoked by policy, social scores, usage rules, or whatever fresh “emergency” the managerial class cooks up next week.

Bitcoin Fixes Settlement

This is where Bitcoin matters, and not in the lazy “number go up” way.

Bitcoin in proper self-custody changes the deepest part of the problem because it gives you money that can settle without ever asking a bank, custodian, payment processor, or correspondent network for permission. No trusted middleman has to update a ledger in your favor. No committee of overpaid hall monitors has to decide whether your wealth is allowed to move today. No institution can rewrite the final settlement layer because your profile, passport, politics, jurisdiction, or transaction history has become inconvenient.

That isn’t a small improvement. That is the whole point. But it is also where many Bitcoiners stop thinking too early.

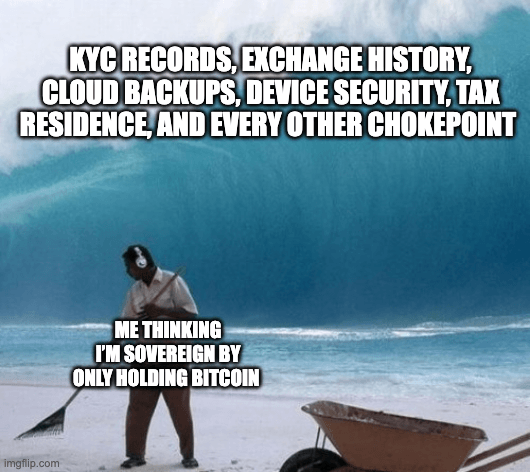

They buy Bitcoin, maybe even take custody properly, and then assume the sovereignty box has been ticked. The coins are off the exchange, the seed phrase is hidden somewhere in their house, the hardware wallet is in a drawer, and suddenly the entire operational footprint of their life has apparently been purified by orange light. Lovely story. Not reality.

Bitcoin can give you final settlement, but it doesn’t automatically erase the trail you left getting there. Your exchange history still exists. Your KYC records still exist. Your bank links still exist. Your email accounts, cloud backups, home network, device security, inheritance plan, tax residence, travel options, family access, and jurisdictional exposure still matter.

This is the difference between owning Bitcoin and building sovereignty around Bitcoin.

The protocol can protect the settlement layer, but it cannot stop a holder from leaking their identity everywhere, storing keys like an absolute lunatic, or pretending the current jurisdiction will remain friendly forever. In reality, they’re actively working to track you down, tighten reporting, and tax you even harder. We covered the direction of travel around exit taxes in The Signal Most People Will Ignore.

Bitcoin removes the deepest monetary chokepoint, but it doesn’t remove every operational chokepoint around the holder. That distinction matters because real life doesn’t attack your setup through the protocol. It attacks through bad backups, sloppy privacy, compromised devices, confused family members, weak inheritance planning, KYC, banking dependency, tax complexity, relocation friction, and the old fatal assumption that tomorrow’s rules will look similar to today’s.

So yes, Bitcoin fixes settlement. But if everything around your Bitcoin still depends on permission, surveillance, fragile custody, poor planning, and one jurisdiction behaving itself, then you have not built sovereignty yet. You have bought the right asset and left too many old doors open around it.

Sovereignty Means Fewer Chokepoints

The fiat system is building more checkpoints, not fewer.

Some will arrive through sanctions, some through tax rules, some through anti money laundering controls, some through “consumer protection”, and some through the shiny CBDC brochures that make surveillance sound like innovation. Different costume, same little dream: more control over who can move value, when, where, and under what conditions.

Bitcoin is the answer to the deepest part of that problem. But serious sovereignty doesn’t stop at owning the asset. It means reducing the number of places where your wealth, identity, custody, inheritance, privacy, and mobility still depend on someone else staying comfortable.

That is the work. Proper custody. Cleaner privacy. Better operational security. Monitoring that helps you detect problems early. Jurisdictional optionality before the exits are crowded. A setup designed for pressure, not just for an ideal version of normality.

Remember, the new border is being built inside the rails. So if you’re serious about sovereignty, your job is to reduce the number of gates it can close around you. And if you want help reviewing those layers before they become urgent, book a free 30-minute introductory call with one of our advisors.