Welcome to Weimar

In this article:

In 1295, Marco Polo came back from China and told Europe a story that sounded completely batshit insane.

He described a monetary system where the emperor printed money from the bark of mulberry trees, stamped it with an official seal, and then threatened to execute anyone who refused to accept it as payment. Paper money enforced at swordpoint. Backed by nothing but imperial decree and the threat of violence. What could possibly go wrong?

To a European audience accustomed to coinage made from gold and silver, this appeared ridiculous, unnatural, and even deceptive. And yet within China, it functioned. Trade continued, obligations were settled, and life proceeded without disruption. From the outside, it looked fragile as hell; from the inside, it felt completely normal.

What followed is less often emphasised. Over time, issuance expanded, confidence weakened, and eventually the system deteriorated alongside the dynasty that sustained it. Turns out paper backed by threats has the same shelf life as the regime enforcing it. Shocker.

Sound familiar yet? Because here we are in 2026 watching the exact same movie, just with better suits and fancier printers. Central banks cranking out endless fiat coupons to fund wars, bailouts, and their own cushy pensions while telling you “inflation is transitory”. Governments keep pretending this mulberry-bark 2.0 is rock solid. And the normies inside the system? They still think it feels normal. Trade continues. Mortgages get paid. Life proceeds without disruption… until it doesn’t.

Monetary breakdown is almost always understood through examples that are safely removed from present experience: Weimar Germany, Zimbabwe, Venezuela, Argentina. Each case is treated as a consequence of particular local failures: poor policy, weak institutions, political instability. This allows it to be categorized as an exception rather than a recurring process.

The effect is subtle but important. It reinforces the belief that such outcomes belong to specific conditions that do not apply more broadly. The conclusion is rarely stated directly, but it is widely implied: that whatever is happening now is fundamentally different.

The Misunderstanding: How Collapse Actually Begins

The difficulty with this reasoning is that it focuses on how these episodes ended rather than how they developed. The defining features of collapse, including visible dysfunction, loss of confidence, and disorder, don’t appear at the beginning. They emerge later, often after the underlying conditions have already been in place for some time.

In those earlier phases, the system continues to function. Prices climb higher, but transactions keep clearing. Debt explodes, yet the markets just swallow it whole. The suits in charge tweak a few dials, everyone nods along, and the comforting lie stays alive: “stability will be maintained”. Nothing appears sufficiently abnormal to justify a fundamental reassessment.

Fast-forward to May 2026, US national debt has slammed into $39 trillion, with net interest payments on track to exceed $1 trillion annually, having already overtaken defense spending. These figures are significant, but they don’t register as indicators of imminent breakdown. They are interpreted as minor speed bumps to be managed within an otherwise stable system.

This is the blind spot. It is not a lack of awareness, but a tendency to interpret developments through the assumption of continuity.

Which is why the more difficult question is not whether such outcomes have occurred elsewhere, but whether we would recognize the early stages if they were unfolding in front of us. Or whether we would assume, as before, that things will stabilize rather than continue to get worse.

It Accelerates Faster Than Expected

The early stages are misread because they feel gradual. The shift that follows is missed because it isn’t.

Monetary deterioration doesn’t move in a nice straight line. It compounds. What starts as a gentle drift can suddenly accelerate into something far uglier once confidence begins to crack.

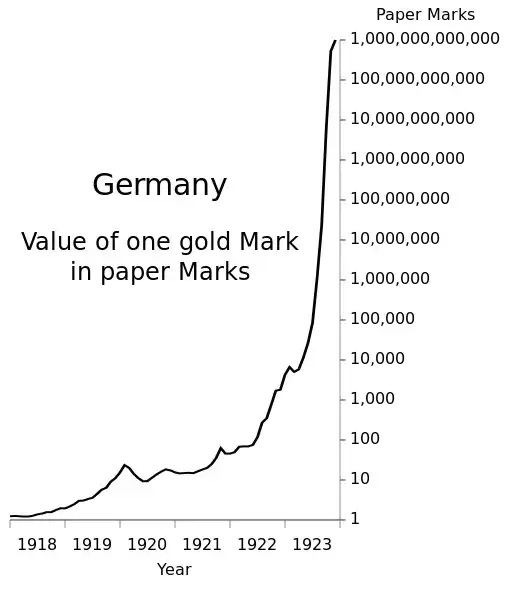

Take Weimar Germany. At first the collapse of the mark was brushed off as a manageable headache that the experts could keep contained. Exchange rates wobbled, prices crept up, and the “experts” kept insisting they had everything under control.

There was no single moment that clearly marked a transition from stability to crisis or where everyone went “good grief, it’s over”. The system appeared to weaken incrementally.

What changed was not simply the level of inflation, but its behaviour. As confidence eroded, the relationship between cause and effect began to compress. Movements that once took months began to occur over weeks, then days. In some cases, even hours.

Fergusson, in his book When Money Dies, recounts a man ordering a coffee for 5,000 marks. By the time he finished drinking it, the price had risen to 9,000. In factories, wages were distributed twice daily so they could be spent before they lost value. Shops adjusted prices constantly, sometimes multiple times within the same day.

This is the point at which linear expectations fail. People project recent experience forward, assuming that conditions will continue to deteriorate at roughly the same rate. But once the underlying dynamics shift, that assumption no longer holds. The system begins to move faster than the models used to interpret it.

And critically, behavior doesn’t adjust fast enough. People continue to act as if time is still on their side, even as the window to respond is narrowing.

The brutal part? This transition is almost impossible to see clearly while it’s happening. It still feels like “more of the same, just a bit worse”. There’s no clear boundary that announces we have entered the nonlinear phase.

Which is why it is so often missed.

The expectation remains that the situation, while worsening, is still fundamentally controllable. So the comforting story continues: sure it’s getting bad, but we can still stabilize it. We just need one more intervention.

But this is the point at which deterioration stops feeling gradual and starts becoming nonlinear. And by the time that shift is widely recognized, the conditions that made earlier responses possible are no longer in place.

"It Can’t Get Worse Than This"

If the previous stage is defined by misreading the pace of change, this one is defined by misjudging its limits. Each deterioration feels like it must be the worst point. Conditions worsen, expectations reset, and what would have seemed unthinkable months earlier becomes accepted as the new baseline.

Prices surge, savings erode, and yet daily life continues in altered form. People carry cash in bulk and find workarounds. What begins as disruption becomes a habit. There’s that famous story from Weimar: a woman who left a wheelbarrow full of banknotes outside a shop while she went inside. When she returned, the wheelbarrow had been stolen, but the money was still there.

The same pattern is visible today. Are we watching this exact farce playing in 2026? Every stage comes with its own predictable government fairy tale, “this inflation is extreme, but largely transitory”. Blame it on the latest emergency: a pandemic, war, supply shock, evil speculators, whatever is convenient this week. The excuse changes, the conclusion never does.

What they will not admit is the real game. The system is deliberately built on endless debt expansion and engineered devaluation of the currency. The government and central bank aren’t incompetent. They are doing exactly what serves their own interests. They get first access to the newly printed money through the Cantillon effect. They spend it before prices rise, and transfer wealth from the productive middle class to the connected elite and the state itself.

Meanwhile, the average person is left adapting to their own slow-motion impoverishment. None of this is treated as evidence of a failing system run by self-serving bureaucrats. It’s simply framed as "challenging conditions" that require more intervention.

Prices keep marching higher and debt is exploding. The government and its central bank partners keep printing and spending in their own interest. What would have been considered monetary malpractice a few years ago is now calmly absorbed as the new baseline.

When Everyone Tries to Leave

For a while, people adapt inside the system.

They accept higher prices, weaker purchasing power, and the latest official explanation for why none of this is quite as bad as it looks. They complain, adjust, and keep moving. The currency is still used because it has to be used. Salaries are paid in it, taxes are demanded in it, and shops still price in it. Life continues around the damage.

But there comes a point when adaptation is no longer enough. The question changes from “how do I manage this?” to “how do I stop holding the thing being destroyed?”. That is the real turning point.

In Weimar Germany, this meant a rush into anything that could hold value better than the mark. Foreign currency, gold, food, coal, property, clothing, furniture, and basic goods all became preferable to money itself. People were not trying to get rich. They were trying to avoid being made poor by simply standing still.

The currency doesn’t fail only because prices rise. It fails because people’s behavior toward the currency changes. They stop seeing it as a place to store value and start seeing it as something to get rid of as quickly as possible.

Today, the cleanest expression of that instinct is Bitcoin. Not a trade. Not a portfolio allocation. Not a speculative hedge for people trying to beat inflation by a few percentage points. It is money outside the machine that is devaluing everything else.

Dollars can be debased. Bank deposits can be frozen. Gold can be difficult to move and secure. Property can be taxed, seized, or trapped inside a jurisdiction. Bitcoin is different: a bearer asset, fixed in supply, portable across borders, and capable of being held without permission.

Once enough people understand what is happening, the issue is no longer personal preference. It becomes a threat to the system itself. A population quietly saving in the currency can be managed. A population trying to escape the currency is a different problem entirely.

At that point, the state does what states always do when control starts slipping. It protects the system, not the individual. The language will be calm and administrative. Financial stability, consumer protection, anti-money laundering, emergency measures, and temporary restrictions. But the direction is always the same: slow the exit, control the rails, manage the flow, and make leaving harder than staying.

That is what happens when everyone tries to leave.

You Can’t Exit Properly

And this is where the trap begins.

Once people start trying to leave at scale, the system drops the polite act. Exits stop being neutral, withdrawals turn conditional, currency conversion becomes restricted. Moving money abroad becomes harder, more expensive, and more visible. Exchange rates split between the official fantasy number and the price people actually pay when they’re desperate to get out of a collapsing currency.

The same logic applies beyond the banking system. When people try to exit financially or geographically, governments do not simply wave goodbye. They add friction, reporting rules. capital controls, and exit taxes. Anything that makes leaving harder, slower, more expensive, or more visible.

We covered this in more detail in The Signal Most People Will Ignore, but the principle is simple: by the time enough people realise they need an exit, the exit is no longer treated as a private decision. It becomes something the state wants to manage.

This is the part people misunderstand. The state doesn’t need to close the door completely. It only needs to control the terms of exit. You can withdraw, but with limits. You can convert, but at the official rate. You can move funds abroad, but with reporting, approvals, taxes, and delays. You can still see your balance, but that doesn’t mean you can use it freely.

Bitcoin in self-custody is different because it gives you direct control over the money itself. Properly held Bitcoin sits outside the banking rails, outside withdrawal limits, and outside the machinery that can decide when, how, or whether you are allowed to access your wealth. But that doesn’t mean governments have no leverage. They can still make escape harder.

The Window Is Only Open Before It Looks Like One

The point is not to predict the exact crisis, the exact date, or the exact trigger. That is how people get trapped in arguments while the structure around them keeps deteriorating. The point is to be positioned before prediction becomes obvious.

Bitcoin gives you the monetary exit. It lets you hold value outside the system built on debt, debasement, and forced participation. But the asset is only one part of the equation. The rest is structure.

Do you actually control your keys? Can your family access your Bitcoin if something happens to you? Are your backups secure without being fragile? Have you reduced obvious exposure? Do you understand the trade-offs between convenience, privacy, inheritance, and physical security? And especially have you thought about jurisdiction before jurisdiction becomes the problem?

These are not details. They are the difference between owning Bitcoin and being truly sovereign. A weak setup does not become strong because the macro environment gets worse. It becomes more dangerous, because pressure exposes every shortcut taken when things still feel calm.

This is where we come in. We help people move from Bitcoin exposure to Bitcoin resilience: proper self-custody, personal security, privacy awareness, and Plan B thinking that holds up when conditions are no longer comfortable.

If you want help building that structure, book a free 30-minute consultation with one of our advisors. We’ll help you secure your Bitcoin properly, reduce your exposure, and build a plan before the window starts to narrow.