The New Counterparty Risk Wears a Bitcoin Logo

In this article:

The most dangerous company in your Bitcoin setup is probably the one you’ve never even heard of.

You don’t see its logo. You don’t follow its CEO on Twitter. You sure as hell don’t think of yourself as its customer. But somewhere behind the clean dashboard, the instant purchase, the wire transfer, or the “Bitcoin-first” brand, there may be another company handling the machinery that decides what your balance actually means. Most Bitcoin holders have never heard of Prime Trust. And that’s exactly the problem.

For years, Prime Trust sat in the background of the industry. It was not the brand most customers saw on the homepage. It was the regulated custody and payments infrastructure underneath other businesses, the kind of company that made the front-end experience feel smooth while handling pieces of the operational machinery behind the scenes.

You might open an account with a Bitcoin company, see a clean dashboard, buy some sats, and think your relationship is with the brand on the screen. But behind that brand there is usually another company holding assets, processing wires, managing accounts, or maintaining the legal structure. Prime Trust was one of those layers. Then, in 2023, it collapsed.

Nevada regulators woke up one day and admitted Prime Trust was short customer funds, couldn’t pay withdrawals, and was basically insolvent. Bankruptcy followed. To most people scrolling the news it was just another post-FTX clown show: sad, predictable, next headline please.

But counterparty risk doesn’t always end when the company fails. Sometimes it keeps moving through the system long after the corpse has gone cold.

The Legal Afterlife of Counterparty Risk

In 2026, the litigation trust created from Prime Trust’s bankruptcy estate began pursuing major Bitcoin-related companies over assets allegedly moved out before Prime filed for Chapter 11. Swan Bitcoin is facing a complaint seeking to claw back roughly $970 million in assets, including nearly 12,000 BTC, cash, stablecoins, and other assets. Strike has also been targeted in a separate clawback action over cash and Bitcoin allegedly withdrawn during Prime Trust’s final weeks.

This isn’t a story about one company. It is a story about a shared custody layer, a failed intermediary, and the legal afterlife of assets that customers may have assumed were already out of danger.

The lawsuits involve allegations, not final court findings. Swan and Strike can argue that they acted properly, that the assets were customer property, and that moving funds away from a failing custodian was necessary to protect users. They may be right. In fact, from the customer’s perspective, that may be the sympathetic reading. But the bigger lesson doesn’t hinge on who gets labeled guilty.

The real problem is this: the moment your Bitcoin touches a third-party custody structure, the risk stops being purely technical and turns legal, operational, contractual, and institutional.

The question is no longer “Where are my coins?” It becomes “Who had legal title? Were the assets truly segregated? What did the custody agreement actually say? Did one party get preferential treatment? What did the executives know? And how much can a bankruptcy estate claw back years later?”. That is the world Bitcoin was designed to route around.

And this isn’t new in the history of money.

The Oldest Trick in Money

Back in 1609, Amsterdam created the Wisselbank, the Bank of Amsterdam, to fix a real mess: Europe was drowning in clipped, debased, inconsistent coins. Merchants needed a reliable settlement layer, so they deposited metal and settled trade through bank money backed by trusted reserves. For a long time, it worked beautifully. The bank became one of the great financial institutions of its age because it gave commerce a cleaner standard than the chaotic coinage around it.

But the wrapper gradually changed the nature of the thing it was supposed to protect. Over time, the bank moved away from the simplicity of full reserve discipline and extended credit, including large advances tied to powerful commercial interests. What began as a trusted monetary utility became another institution shaped by discretion, secrecy, political pressure, and balance-sheet risk.

Sound familiar? It’s the exact same script today’s central banks are still running, “we’re just here to stabilize things” and then end up printing their way to serfdom while calling it sophisticated monetary policy.

The ending was slow, but the lesson was brutal. The Bank of Amsterdam didn’t collapse because gold and silver failed. It failed because the institution built around them quietly broke the discipline that made it trustworthy in the first place. It lent against reserves, became entangled with powerful commercial interests, hid the damage for too long, and eventually had to admit insolvency. By 1790, confidence had cracked. By 1791, the city had taken control. The wrapper built to protect gold and silver had become the risk.

Sound money attracts wrappers because people want convenience. Wrappers attract trust because people prefer dashboards to responsibility. Trust attracts complexity because institutions discover they can do more with other people’s assets than simply hold them. Eventually, the simple question of ownership becomes buried under agreements, ledgers, exemptions, liabilities, and lawyers. That is why Prime Trust matters. Not because it broke Bitcoin. It didn’t.

It matters because it reminds us that a Bitcoin company can speak the language of sovereignty while still depending on infrastructure that brings old-world counterparty risk back into the room. The customer sees the Bitcoin brand. The legal system sees custodians, claims, transfers, creditors, preference windows, and bankruptcy estates.

Those are very different worlds. And when things go wrong, it is usually the second world that decides what happens next, because this is what custodial Bitcoin does. It moves the centre of gravity away from keys and into contracts, records, claims, creditors, and legal interpretation.

When Bitcoin Becomes a Product

Prime Trust is the textbook custody version of the trap. A “trusted” institution hides in the plumbing underneath the shiny product. Customers see the clean front-end dashboard, click “buy Bitcoin,” and feel like they’re stacking real sats. Then the hidden layer blows up and everyone suddenly discovers that “your balance” was never quite as simple as the pretty interface made it look. But custody is just one flavor of wrapper.

There are other wrappers now. Public companies. Treasury vehicles. Lending products. ETFs. Managed accounts. “Bitcoin income” strategies. Balance-sheet plays dressed up as sovereignty. Each one offers something people want: convenience, liquidity, a little yield, institutional access, or the warm fuzzy feeling of never having to touch your own private keys again. And that is why they keep growing.

The appeal is easy to understand. Self-custody asks people to accept responsibility without a reset button. A wrapper softens that burden. It turns bearer money into an account, a ticker, a product, a line item, or a professionally managed strategy.

Sure, it might feel useful at the moment. But it is never neutral. Every single wrapper brings its own set of incentives and landmines. A treasury vehicle has management teams, dilution risk, reporting deadlines, and the constant need to keep the shareholders happy. The asset underneath may still be called Bitcoin, but the thing you actually own is no longer just Bitcoin. It’s a Bitcoin IOU, plus a whole new layer of counterparty theater.

That is where Nakamoto enters the story. Not as another Prime Trust case, but as a different warning from the same family: once Bitcoin becomes part of a corporate machine, the risks start to look less like self-custody mistakes and more like public-market finance.

Bitcoin Doesn’t Need a Reverse Split

Nakamoto (NAKA) should have been the easiest story in the world to “sell”.

A public company with the most sacred name in Bitcoin. Few thousands of BTC on the balance sheet, David Bailey at the centre, and loaded with media assets, conference machinery, and deep industry connections.

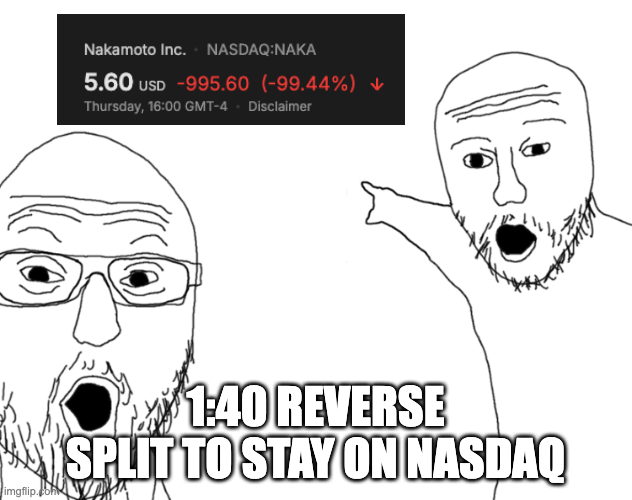

By May 2026, NAKA had fallen roughly 99% from its May 2025 peak of more than $34, with shares trading near $0.2. That pushed the company into one of Wall Street’s least dignified manoeuvres: a reverse stock split. Nakamoto confirmed a 1-for-40 reverse split, effective May 22, to help regain compliance with Nasdaq’s $1 minimum bid requirement. The move reduced outstanding shares from roughly 696.1 million to about 17.4 million.

The reverse split doesn’t fix the business. It doesn’t restore trust. It doesn’t create new value. It takes forty wounded shares, staples them together, and asks the market to pretend the limp is gone. That may satisfy the exchange but it doesn’t satisfy reality. The split did what it was mechanically supposed to do: it lifted the quoted share price. But it did not change the market’s judgement. NAKA closed at $7.23 on its first split-adjusted trading day, fell to $5.49 the next trading session, and was around $5.05 the following day. In other words, even after the financial cosmetic surgery, the stock gave up roughly 30% in just a few sessions.

The quarterly filings only made the picture uglier. In Q1 2026, Nakamoto reported a few million dollars of revenue against a $238.8 million net loss. To keep the lights on, the company sold 284 BTC while running derivatives strategies that generated more Bitcoin; only to sell that as well.

This was never really Bitcoin. It was a corporate wrapper using actual Bitcoin as collateral for an entirely different story. And like every wrapper, it brought its own set of incentives that pure Bitcoin would never tolerate: dilution mechanics, acquisition accounting games, hefty compensation structures, related-party complications, Nasdaq compliance pressure, conference economics, media politics, and the perpetual need to convince investors that the packaging was more valuable than the coins sitting underneath it.

Because this is where the contradiction becomes obvious. Bitcoin teaches scarcity, while public companies can issue more shares. Bitcoin teaches verification, public companies ask you to read filings and trust management. Bitcoin teaches self-sovereignty, while treasury companies sell exposure.

That doesn’t mean every Bitcoin company is useless. It means the wrapper must be judged as a wrapper. Not as Bitcoin. Not as a moral substitute for custody. Not as some sacred extension of the protocol because the branding happens to be orange.

Nakamoto’s collapse in market value doesn’t make Bitcoin weaker. It makes the lesson sharper. A company can wrap itself in Bitcoin language, own real BTC, speak to Bitcoiners, host Bitcoiners, publish to Bitcoiners, and still behave like a public-market machine once the incentives take over.

And public-market machines have one habit Bitcoiners should understand by now. They always find a way to print.

Services Are Tools, Not Sovereignty

Look, the point isn’t that every Bitcoin company should be avoided. That would be lazy and dishonest.

Good services matter. Most people are not going to build a secure custody, backup, inheritance, cybersecurity, and monitoring setup alone. Families need help. High-net-worth holders need guidance. Busy professionals need someone to show them where the real risks are before those risks become expensive.

The problem starts when the service becomes a substitute for understanding.

A custodian can be useful, but it isn’t self-custody. A treasury stock can provide exposure, but it isn’t Bitcoin in your control. A lending product can unlock liquidity, but it isn’t free money. Your Bitcoin becomes collateral, and collateral lives under someone else’s terms: margin calls, liquidation thresholds, repayment schedules, and fine print. A dashboard can show a balance, but it isn’t the same thing as holding keys. A company can be Bitcoin-first and still sit between you and Bitcoin. This distinction is everything.

Bitcoin gives you the ability to own an asset without asking permission from a bank, broker, exchange, custodian, government, or payment company. But that ability only matters if your setup preserves it. If convenience moves control back to someone else, the branding can stay orange while the risk turns fiat again.

Every serious holder needs to constantly ask two brutally honest questions: Where is this company actually making me stronger with Bitcoin? And where is this company just becoming the new trusted third party I’m supposed to believe in?

Because once you cross that line, you’re not stacking Bitcoin anymore. You’re just stacking someone else’s IOU with better marketing.

Your keys. Your coins. Your rules.

But those words only mean something if the setup behind them is real. That means knowing where your Bitcoin sits, how your keys are secured, how your backups are protected, what happens if you’re unavailable, and whether obvious weak points have been removed before they become expensive.

Whether you need realtime wallet monitoring, a cleaner self-custody structure, or a review of your current process, you don’t need to figure it all out alone. If you’re ready to take proper custody for the first time, or you want to strengthen the setup you already have, book a free 30-minute introductory call with one of our advisors.