The Tide Turns Before the Price Does

In this article:

There’s a peculiar kind of amnesia that kicks in the moment Bitcoin trades sideways for a while.

People who were calling it a monetary revolution six months ago suddenly start treating the four-hour chart like it’s the only thing that matters. Search interest drops, timelines go quiet, the tourists drift off towards the SpaceX IPO, the latest AI miracle or whatever shitcoin is promising generational wealth by next Thursday. Before long the verdict comes in: momentum is gone, conviction is fading, and Bitcoin has apparently become less important because the candles stopped making people feel clever.

A censorship-resistant monetary network reduced to an emotional support chart for people with TradingView accounts. Price rises and the future feels inevitable. Price stalls and the entire thesis apparently requires urgent review. Public excitement becomes a proxy for adoption, while social-media noise is mistaken for conviction, even though both are among the least reliable signals available.

They are watching the waves and assuming they understand the ocean. Waves announce themselves. They arrive with green candles, corporate announcements, political promises and television experts suddenly remembering that Bitcoin exists. They carry traders, tourists and freshly minted monetary philosophers towards the shore, where everyone begins discussing freedom shortly after checking how much richer freedom has made them.

Then the wave retreats. The headlines thin out, the memes become less frantic and those who mistook attention for belief start announcing another death. From the surface, the movement appears to be losing force.

The tide behaves differently. It moves underneath everything, slower and far more stubborn. You notice it when the questions begin to change. Someone who once asked how high Bitcoin could go starts asking why a bank can delay the movement of their own money. Someone drawn in by speculation begins wondering why their savings lose purchasing power while the people responsible describe the process as stability. Someone who bought through an exchange gradually realizes that seeing a balance on a screen and owning Bitcoin are two very different experiences.

These changes tend to begin after the existing system delivers one of its small, unsolicited lessons.

The System Keeps Making the Case for Bitcoin

A transfer gets delayed. An account falls into review. Another document is requested. A currency weakens while political puppets and their central-bank puppeteers insist everything is under control, as though repeating the lie slowly enough might restore your purchasing power. A government discovers that the latest emergency requires more debt, more monitoring and a few additional restrictions for everyone’s protection.

Each incident appears ordinary when viewed alone. Together, they create a psychological crack. The person affected may still lack the vocabulary of monetary sovereignty, but the deeper question has already begun to form: why should access to my own wealth depend on institutions whose rules can change whenever they become frightened, pressured or politically instructed?

This question matters more than another round of market excitement because it changes what Bitcoin represents. Greed will continue to bring people through the door, and it remains one of history’s most reliable recruitment tools. Plenty of people first buy Bitcoin because they want more fiat, an earlier retirement or the private satisfaction of becoming unbearable at family dinners.

The real shift happens when the person hoping to escape work starts thinking about escaping dependence instead. Price still matters, obviously. Nobody buys something hoping it goes down, no matter how philosophical they later pretend to be on Twitter/X. But the number gradually stops being the whole story. Bitcoin stops being just a bet on getting richer and starts becoming a practical answer to a question the current system keeps making harder to dodge: why should anyone else have this much control over my money?

No chart can measure the moment that question takes hold. It appears in the person learning self-custody after years of trusting an exchange. It appears when a family finally discusses inheritance before incapacity or death turns confusion into disaster. It appears when someone begins thinking about privacy, jurisdiction and financial resilience rather than waiting for the next price target to restore their conviction.

From the outside, this can look like silence. Genuine conviction usually does. It lacks the theatrical energy of a bull market because people building competence rarely interrupt themselves every six minutes to post a rocket emoji. That is why the current mood is so easy to misread.

The surface feels calmer because the speculative noise has faded, yet beneath it more people are beginning to understand what Bitcoin is actually for. They are arriving not only through inflation, but also for surveillance, broken trust, political uncertainty and the slow realization that permissioned money belongs to them only while every institution standing between them and it remains cooperative.

When The Plebs Stopped Asking Nicely

Rome faced a very different crisis more than two thousand years ago, but the pattern beneath it was already familiar.

By 494 BC, barely fifteen years after the Republic was founded, the plebeians were living under a system designed by and for the patrician class. Debt could strip them of their land, their freedom, and sometimes their families, while real power stayed with the people who profited most from the arrangement. Rome called this order. The plebs experienced it as something else entirely.

They complained, petitioned and endured, which is usually the stage powerful institutions prefer. Frustration can be managed, anger can be redirected and a population that still believes relief must come from above remains safely dependent on the people standing above it.

Then, in 494 BCE, the plebs realized that Rome needed them too. They supplied soldiers, labour, food and much of the machinery that kept the young Republic functioning, so they withdrew their cooperation and left the city in what became known as the first Secession of the Plebs. The ruling class could keep its grand titles, sacred traditions and impressive collection of togas, but governing without much of the workforce and army proved slightly less satisfying than expected.

The walkout forced concessions, including the creation of the tribunes of the plebs, representatives who could defend plebeian citizens against abuses of patrician power. The plebs had moved beyond asking their rulers to behave more fairly. They had created leverage that relied less on their rulers feeling generous. That struggle continued for more than two centuries. Further secessions followed, and by 287 BC the Lex Hortensia made decisions passed by the plebeian assembly binding across Roman society. What began as anger over debt and exclusion had gradually become a transfer of political power.

That is where frustration becomes dangerous. Most people begin by wanting the existing system to work better. They want banks to stop interfering, politicians to spend responsibly and central bankers to preserve the value of the currency entrusted to them. These are reasonable requests, which may explain why they are treated with such consistent contempt.

Bitcoin introduces a different possibility. Instead of waiting for the monetary patricians to develop restraint, people can begin withdrawing part of their dependence from the system they control.

The comparison only goes so far, obviously. Bitcoiners aren’t marching up a Roman hill with hardware wallets held aloft, and holding a few million sats doesn’t make anyone Spartacus. The psychological move, though, is strikingly similar. People stop asking only how power might be exercised more gently and start asking why so much power was handed over in the first place.

Prague Was Where the Tide Broke the Surface

Modern secessions rarely involve an entire population marching out of a city. They happen more quietly, as people begin moving their savings, attention and trust away from institutions that once appeared unavoidable. The old system remains standing, complete with marble buildings, official seals and politicians confidently explaining its permanence, while dependence starts leaking elsewhere.

Bitcoin was built for precisely that kind of withdrawal. Satoshi released the protocol and then disappeared, leaving behind no chief executive, official spokesman or monetary high priest whose approval the network required. There was nobody left to flatter, lobby, arrest or wheel out in front of cameras whenever the price needed emotional support. The system carried on because it had been designed to outgrow its creator and offer anyone, anywhere, a peaceful route towards monetary independence.

Bitcoin in self-custody became the ticket to freedom. BTC Prague showed how many more people are beginning to understand what that ticket is actually for. By the usual market logic, the conference should have felt quieter. The price lacked the narcotic energy of a fresh all-time high, the tourists had fewer reasons to photograph themselves beside orange logos and the chart had stopped issuing daily permission slips for optimism.

Instead, attendance reached an all-time high and the venue was overflowing with people who had arrived without requiring the market to seduce them first. Prague felt different for that exact reason. For a broader look at the speeches, conversations and moments that made BTC Prague such a powerful event, read our full conference recap here: Freedom, Responsibility and a Weekend to Remember in Prague. The energy came from people who increasingly understood that Bitcoin offers more than a chance to get wealthier inside the existing system. It offers a way to become less dependent on it.

The contrast on the main stage made that shift difficult to miss. Saylor spoke before Tony, bringing the enormous numbers, digital-capital framework and corporate language that have made him Bitcoin’s most recognizable translator to the institutional world. That framework has helped institutions understand Bitcoin, although it can also shrink a monetary revolution into better collateral for the same financial machine. Bitcoin becomes something to borrow against, wrap in digital credit and feed back into a system built on leverage, intermediaries and promises somebody else must honor.

Then Tony walked onto the same stage and took the argument beyond the balance sheet. He said that money no longer needs the state and no longer has to obey it. He paused, repeated the line and the response grew louder, because the audience understood that he was describing something far larger than another investable asset. He was describing an escape route. You can watch Tony’s full keynote here.

The conversations moved beyond price projections, digital credit and corporate adoption towards custody, competence, privacy, and the responsibility attached to genuine ownership. People were asking what freedom requires once the applause stops and sovereignty follows them home, where their devices, backups, families and operational mistakes are waiting to examine how seriously they meant it.

Saylor remained important, but he no longer consumed the entire gravitational field. The audience could absorb his case and then continue towards the harder questions Tony had placed before them: who controls your money, what makes it truly yours and what kind of person must you become once nobody else is responsible for protecting it?

That is what winning looks like. Winning isn’t another famous person saying something bullish or another company adding Bitcoin to its treasury. Those victories may matter, although they remain visible waves on the surface. The deeper victory arrives when people stop waiting for institutions to validate Bitcoin and begin using it to reduce their dependence on those institutions. It arrives when they understand that Bitcoin in self-custody is more than an investment. It is their ticket to freedom.

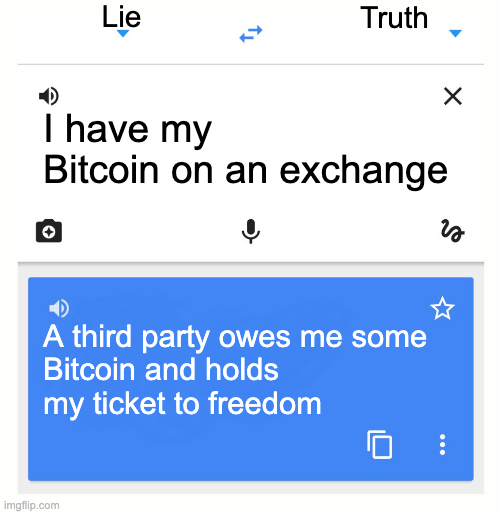

A Ticket Is Useless If Someone Else Holds It

There is one uncomfortable problem with calling Bitcoin a ticket to freedom. A ticket sitting in someone else’s wallet still leaves them deciding whether you get through the gate.

That is why the shift from speculation to sovereignty matters so much. Plenty of people understand that Bitcoin can protect them from monetary debasement while continuing to hold it through an exchange, a custodian or some beautifully designed app that promises ownership right up until its lawyers discover a more creative definition.

The idea has reached them. The responsibility has not. Self-custody closes that gap, although holding your own keys is only the beginning. Freedom quickly becomes practical. Can you recover your Bitcoin if a device fails? Can your family access it if you die? Does your setup protect your privacy, or does it broadcast enough information to make every future decision easier for somebody else? Have you built resilience, or simply moved the same blind trust into a cold wallet?

These questions lack the emotional thrill of a price prediction, which is precisely why they matter. The crowd in Prague understood that money no longer needs the state. The next stage is understanding that sovereignty cannot be outsourced to an exchange, delegated to a custodian or improvised by grieving relatives after the keys disappear with you.

Winning means becoming harder to control without becoming easier to rob. It means building a setup that survives mistakes, emergencies and changing circumstances. It means thinking about inheritance before your family needs it, privacy before exposure becomes a problem and jurisdiction before the rules tighten around you.

The tide may be turning, but it will not carry anyone to freedom automatically. You still have to learn how to sail. Fortunately, you do not have to walk that path alone or improvise your way through it with a few YouTube videos and misplaced confidence. When your entire Bitcoin stack is on the line, even a small mistake can become a very expensive lesson. If you are serious about protecting your Bitcoin properly, book a free 30-minute introductory call with one of our advisors.